While the concept of unearned revenue as a liability is primarily relevant to corporate accounting and asset management, it also indirectly intersects with wealth management when evaluating investments that form part of a client’s portfolio.

For wealth managers, understanding that a company’s balance sheet includes liabilities such as unearned revenue is crucial when assessing the quality and stability of a client’s holdings in stocks or bonds. Even though the client doesn’t directly deal with unearned revenue, it affects the valuation, cash flow projections, and risk profile of companies in which they are invested.

By incorporating this insight, wealth management professionals can make more informed decisions, helping clients achieve long-term financial goals while managing exposure to potential risks in their investment portfolio.

Yes, unearned revenue is a liability, and understanding why is key for anyone interested in finance or business accounting. When a company receives money for a product or service it hasn’t delivered yet, that cash doesn’t represent immediate income. Instead, it represents a promise an obligation to provide goods or services in the future. Until the company fulfills that promise, it can’t recognize the cash as earned revenue, so it is recorded as a liability on the balance sheet.

Think of it like paying for a one-year magazine subscription upfront. You hand over your money today, but the publisher hasn’t delivered all twelve issues yet. That payment is a liability for the publisher because they are obligated to provide the remaining issues. Only as each issue is delivered does a portion of the unearned revenue convert into earned revenue, reflecting that the company has fulfilled part of its obligation.

From an accounting perspective, the treatment of unearned revenue aligns perfectly with the accrual accounting principle, which states that revenue should only be recognized when it is earned. Receiving cash before earning it would inflate income and distort financial statements. By recording unearned revenue as a liability, businesses provide a clearer picture of their obligations and avoid misleading investors, creditors, and other stakeholders.

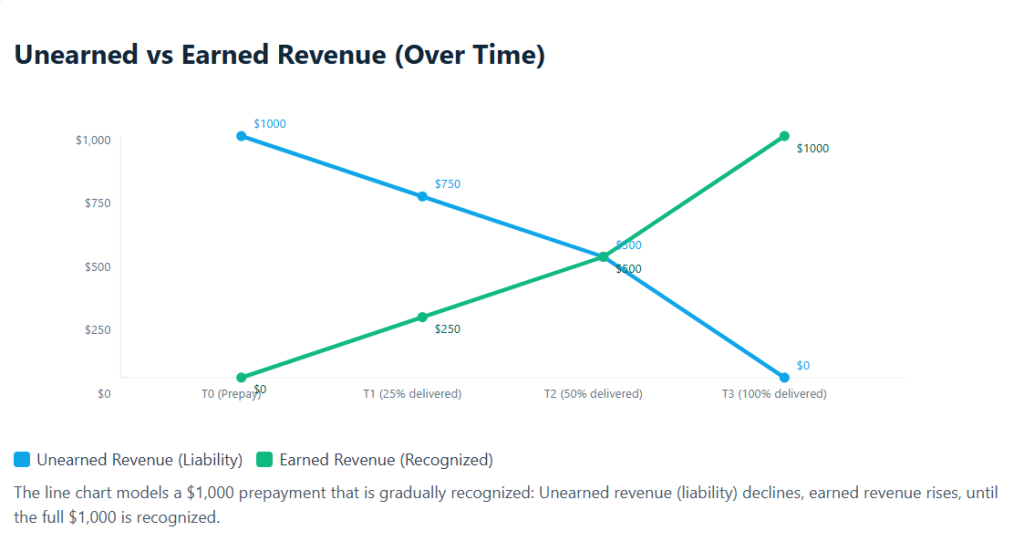

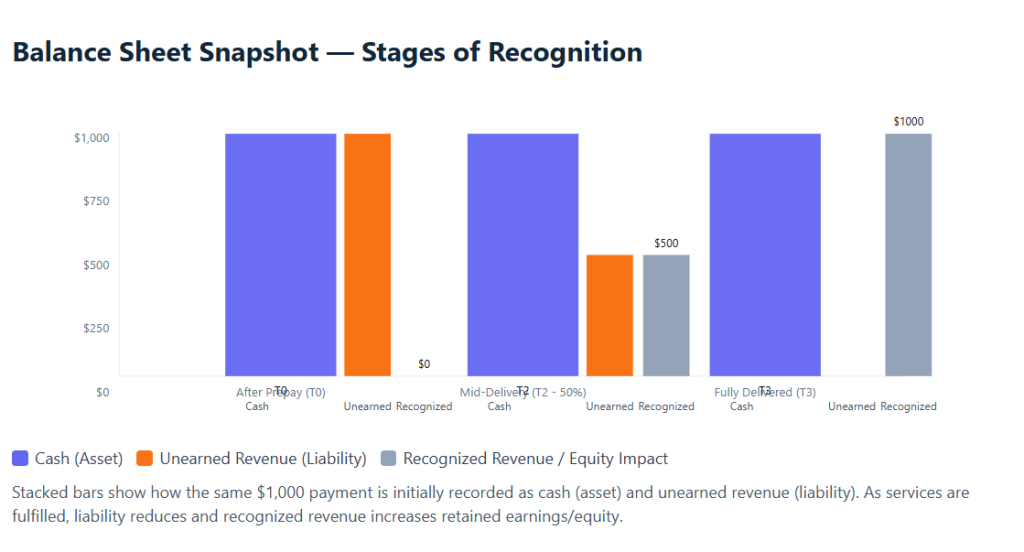

A simple example helps visualize this. Suppose a customer prepays $1,000 for a six-month software subscription. Initially, the company records: Dr Cash $1,000, Cr Unearned Revenue $1,000. Here, cash increases as an asset, and unearned revenue increases as a liability. No revenue appears on the income statement yet because the service hasn’t been delivered.

As the service progresses, say after three months, the company has delivered half of the subscription. At this point, $500 of unearned revenue is recognized as earned revenue. The journal entry would be: Dr Unearned Revenue $500, Cr Revenue $500. The liability decreases, and the income statement reflects the revenue earned. This step-by-step recognition is what makes unearned revenue both a liability and a future revenue stream.

Industries that rely heavily on subscriptions or advance payments frequently report large unearned revenue balances. SaaS companies, insurance providers, airlines, and gyms often have significant deferred revenue because customers pay for services in advance. These balances are important indicators of upcoming revenue, and while technically a liability today, they are essentially a promise of predictable cash flows in the future.

The balance sheet treatment of unearned revenue also helps investors and analysts evaluate a company’s financial health. Large unearned revenue might indicate strong customer demand and recurring revenue streams, but it also signals obligations the company must meet. Investors appreciate transparency here because it distinguishes between cash the company can freely use and cash that is tied to future delivery obligations.

It’s also worth noting that unearned revenue is typically classified as a current liability if the goods or services will be delivered within 12 months. Longer-term obligations are recorded as non-current liabilities. This classification ensures that stakeholders understand the timing of the company’s responsibilities and can accurately assess liquidity and operational risk.

Over time, unearned revenue decreases as services are provided, moving from the liability section of the balance sheet to the revenue line on the income statement. This transition illustrates the dynamic nature of deferred revenue: it starts as a liability but eventually becomes part of the company’s recognized income, contributing to net profit. Monitoring this movement is crucial for effective financial planning and forecasting.

In essence, unearned revenue is a liability because it represents an obligation to deliver value to customers in the future. However, it is not a negative sign; rather, it demonstrates customer trust, future revenue potential, and operational momentum. Proper accounting ensures transparency, avoids overstating earnings, and gives both internal management and external investors a realistic view of the company’s financial position. Understanding this concept is foundational for anyone managing or analyzing business finances.

Visual Explanation of Unearned vs Earned Revenue

Balance Sheet Snapshot of Unearned vs Earned Revenue

Example Journal Entries & Balance Effects

| Stage | Journal Entry | Assets | Liabilities | Income Statement |

|---|---|---|---|---|

| Prepayment (T0) | Dr Cash $1,000 Cr Unearned Revenue $1,000 | Cash +$1,000 | Unearned Revenue +$1,000 | No revenue recognized |

| Partial Delivery (T2 – 50%) | Dr Unearned Revenue $500 Cr Revenue $500 | No change | Unearned Revenue -$500 | Revenue +$500 (recognized) |

| Full Delivery (T3) | Dr Unearned Revenue $500 Cr Revenue $500 | No change | Unearned Revenue -$500 (now $0) | Revenue +$500 (total $1,000) |

These entries demonstrate why unearned revenue is classified as a liability and how it transitions to recognized revenue as obligations are fulfilled.

Final Thoughts : Here is Why You Need to Have an Clear Understanding About Unearned Revenue

Understanding unearned revenue and why it is classified as a liability is more than just an accounting exercise — it provides valuable insight into a company’s financial health, obligations, and future revenue streams. For investors, asset managers, and even wealth management professionals, this knowledge helps make more informed financial decisions. Key reasons it’s important to know about unearned revenue include:

- Accurate Financial Assessment: Knowing that unearned revenue is a liability helps evaluate a company’s true financial position and net assets.

- Revenue Recognition Timing: It clarifies when revenue can be legitimately recorded, preventing overstatement of profits.

- Cash Flow Insights: While cash is received upfront, services or goods are owed, so understanding unearned revenue is critical for predicting future cash flows.

- Investment Analysis: For wealth management and portfolio decisions, recognizing these obligations helps assess the stability and risk of companies in which clients invest.

- Operational Planning: Companies can plan resources, staffing, and production based on deferred obligations reflected in unearned revenue.

- Transparency for Stakeholders: Accurate reporting builds trust with investors, creditors, and clients by showing both assets and obligations clearly.

In short, awareness of unearned revenue as a liability ensures that both professionals and investors interpret financial statements correctly, anticipate future obligations, and make smarter, more strategic decisions.